I’ve found this a difficult newsletter to write. For much of the day, it was hard to think of anything other than the astonishing goings-on in British politics. Then, as I was finishing it, came the shocking news of the shooting of former Japanese Prime Minister Shinzo Abe.Matters of profit and loss pale in comparison with matters of life and death.Markets continue to churn. In a few hours as I write, the publication of US non-farm payroll data for June will give people all kinds of excuses to buy and sell things. The central question confronting the world of investment continues to be the state of the US economy, and the impact the employment market has on inflation; at this point, there isn’t long to wait. Share with The Post: What’s one way you’ve felt the impact of inflation?

While we anticipate some important data, and try to deal with the gravity of events, it’s easy to miss good news. So, let me offer a few reasons for optimism that it has been easy to overlook.

China’s Stimulus

Bloomberg has a scoop that China is contemplating a direct stimulus to its economy by bringing forward $220 billion in bonds issuance to back infrastructure. You could take this as tacit confirmation that the economy is in trouble. It’s a return to the old strategy of pumping up construction spending whenever growth is running out of steam. And it’s only a matter of bringing forward spending that had already been planned; the idea is that local governments building projects can now access financing that would not otherwise have been available to them until next year.

However, the plan also shows that the authorities are prepared to relent in the face of signs that local governments are using the financing that’s there. If they’re prepared to go back to an old playbook that worked, that’s fine by global investors. This graphic from my colleagues illustrates what is going on:

Plenty of bearish arguments hinge on the notion that Chinese authorities are resolved not to resort to a major priming of the pump. Any sign that they are growing less conservative is welcome. There are other unmistakable signs that China’s economic deceleration after renewed Covid shutdowns early this year hasn’t been as bad as feared. Its domestic stock market is surging back, even as the rest of the emerging world is falling back.

There are reasons for this. The strong dollar is seriously problematic for the rest of EM, but less so for China. The country’s entire experience of the pandemic is out of alignment with the rest of the world. The acute selloff for the commodities that China traditionally gobbles up, such as copper, shows the degree of concern. So if the Chinese government really is prepared to pick up the pace again, that will help far beyond its shores. It’s at least worth watching.

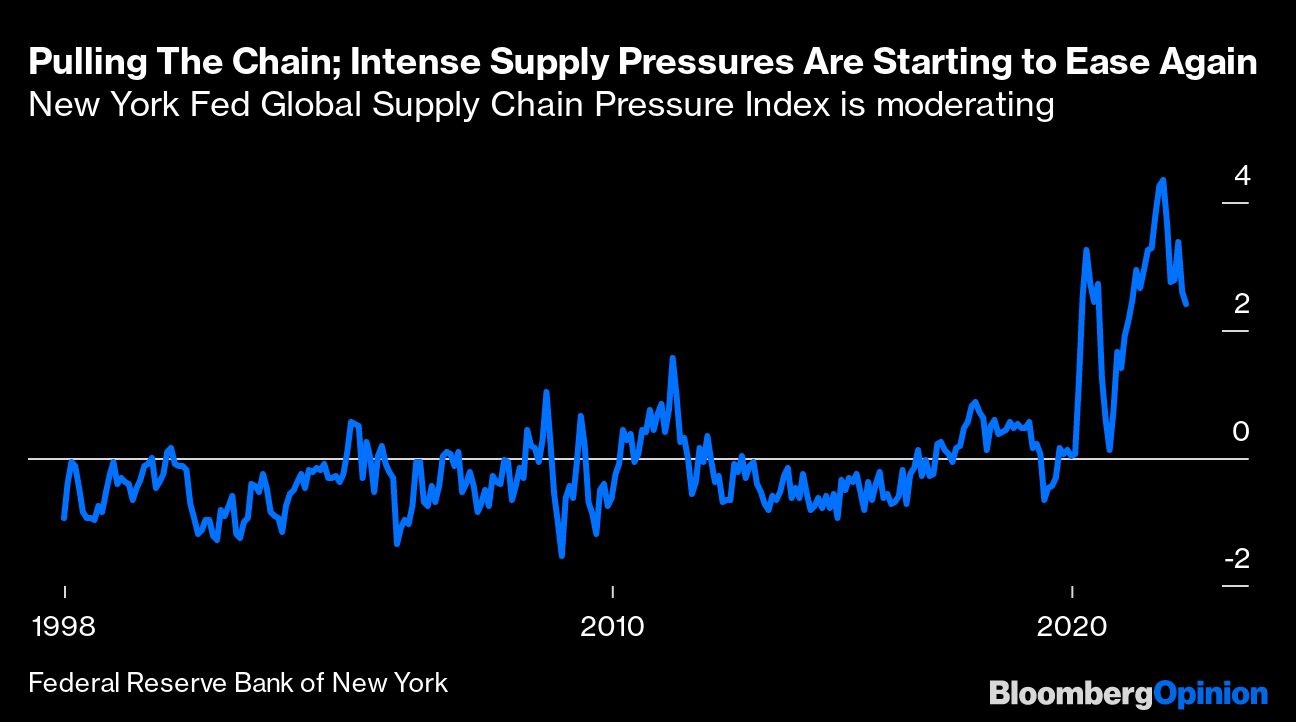

Supply Chains

Inflation owes a lot, if not everything, to stretched supply chains. This problem is beyond the reach of central banks, but still threatens to make the task of monetary policy far harder by embedding inflationary pressure and prompting higher wage demands.

On this issue, there is again some good news. The New York Fed now keeps an index of global supply chain pressure, which smooshes together shipping and freight costs and other measures of how swiftly supply chains are moving. Theserose sharply in 2020, declined, and then surged once more as fresh Covid-19 lockdowns affected activity, particularly in China.

The latest version of the index shows that pressure remains elevated, but is unmistakably declining:

This doesn’t mean the issue is over. It does, however, suggest that one of the world’s most acute problems is beginning to ease. Which is reason to be cheerful.

Covid-19

We all know from personal experience that the pandemic hasn’t gone away altogether. It’s still around, grumbling away as a problem that diminishes quality of life. But at a global level, Covid-19’s ability to take lives really does appear to have been curtailed. These are the latest global numbers as reported to Johns Hopkins University. Omicron was a savage wave, but in its wake the pandemic’s death toll has declined as never before. Nobody will say that it’s over with any confidence after the false dawns of the last two years, but it’s hard to see how anyone could hope for numbers much more encouraging than this, particularly after the horrors of omicron at the turn of the year:

Incidentally, it’s interesting to note that deaths peaked and started to decline exactly at the point when vaccines began to roll out. There is no proof of cause and effect, of course, but there’s a widespread mantra now that vaccines “don’t work.” The facts suggest otherwise. On the critical issue of keeping alive, the circumstantial evidence suggests they’ve worked very well indeed.

Put together a China prepared to prime the pump again, easing supply chains, and the most promising signs yet that Covid can be controlled, and that’s a case for the global economy to perform much better than most assume over the rest of this year.

Keep these thoughts in mind as you brace for Payrolls Friday.

Errata

If you want to read the research paper on factor investing under inflation by Robeco that I mentioned Thursday, you will need to look for it at this link, and not the one I previously offered. My apologies.

Also, in an error that amazingly only one reader appears to have spotted, I butchered a chart of the differential between US and German 10-year yields. I said it had been eliminated. It hadn’t. The point that the gap between 10-year yields has narrowed while the gap between two-year yields has widened remains intact, but the correct chart (below) of the gap in 10-year yields is much less dramatic than I made it appear. Again, my apologies.

Survival Tips

I’m writing this immediately after hearing the Abe news. It puts the fate of Boris Johnson, whose resignation address struck me as lacking in contrition and saturated with self-pity and entitlement, into a cruel and worthwhile perspective.

It also puts the note I was planning to write, on the pleasures of watching Wimbledon in high summer, into a pretty harsh perspective. I’ll press on, because at times like this it’s especially important to seek comfort. Tennis has charms to soothe the troubled brow, particularly when it takes placee in the cheerful greenness of south-west London. It’s a good idea to unwind and get your fill of it this weekend. Some of my favorite matches from the past: Bjorn Borg and John McEnroe’s 22-minute tiebreaker in the 1980 final; Borg vs. the late Vitas Gerulaitis in the 1977 semifinal; and Rafael Nadal dethrones Roger Federer in the 2008 final — you can watch either the whole six-hour event, or these edited highlights, or these very edited highlights. Plus here’s Serena Williams at her imperious best in 2015, and, to prove that it happened once, losing to Maria Sharapova for the last time in a major, in the final of 2004. I will be traveling next week, and probably not sending a newsletter each day. Have a good weekend everyone, and enjoy next week.More From Other Writers at Bloomberg Opinion:

• Abe’s Shooting Stuns a Country Known for Safety: Gearoid Reidy

• Billionaires Can’t Get Enough of Private Equity: Shuli Ren

• Verdict on Johnson’s Prime Ministership Is Mixed: Bobby Ghosh

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

John Authers is a senior editor for markets and Bloomberg Opinion columnist. A former chief markets commentator and editor of the Lex column at the Financial Times, he is author of “The Fearful Rise of Markets.”